Volatility Pulse - Tale of Two Markets

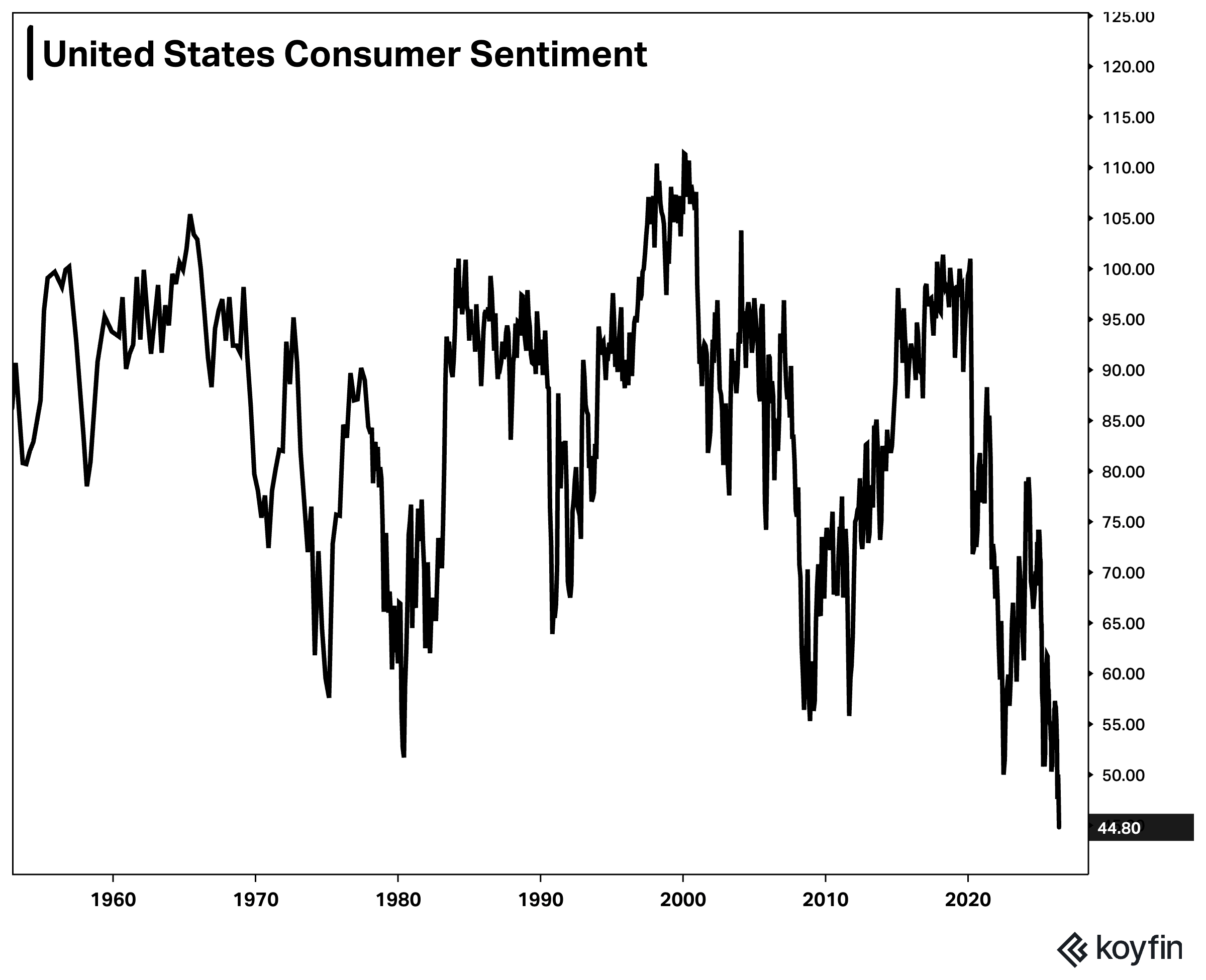

Consumer Mood: Record Low

Michigan Sentiment hit 44.8 this month — the lowest reading in over 70 years of data — while the S&P simultaneously posts an 8-week win streak. The gap between Wall Street reality and Main Street reality has never been wider.

Source: UMich

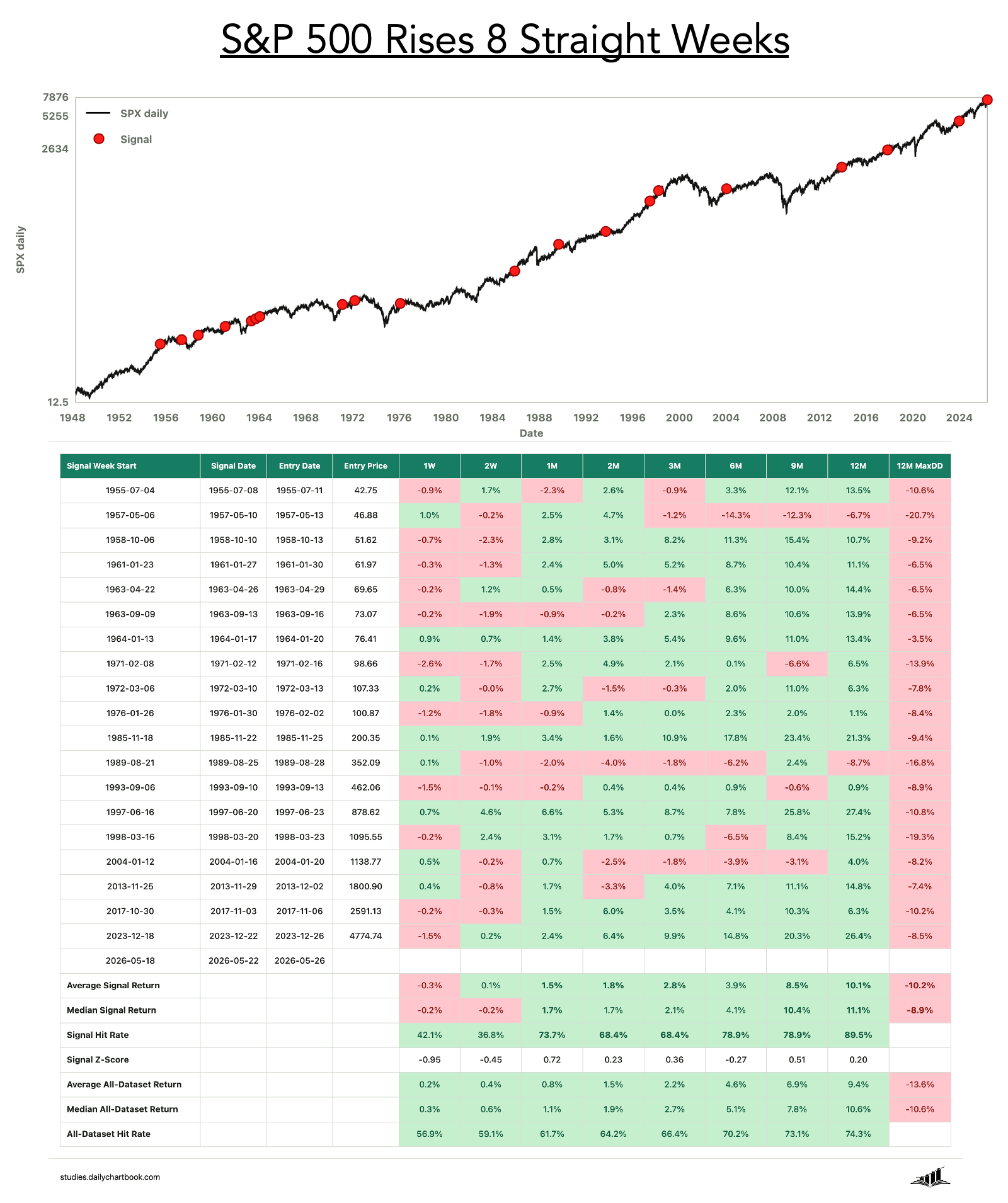

8 Weeks, Hollow Inside

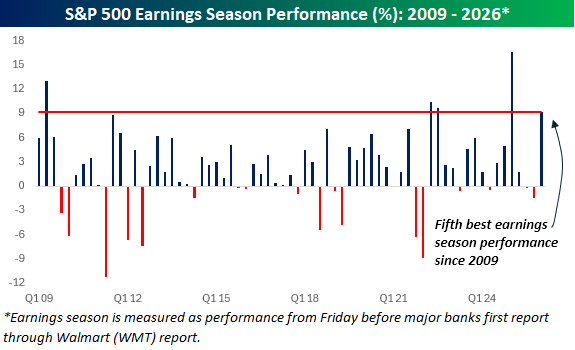

Earnings Season: 5th Best Since 2009

The S&P 500's 9.2% gain during this earnings season ranks as the fifth best since the GFC — just behind Q4 2022, Q4 2020, Q1 2019, and Q3 2009. Beats have been broad, and the market chose to believe them.

Source: FactSet

20th Time Since 1950

The S&P 500 has now risen for 8 consecutive weeks — only the 20th time in 76 years of data. After prior 8-week streaks, the index was higher 12 months later in 14 of 19 cases. History is on the bull's side. So is concentration.

Source: Ned Davis Research

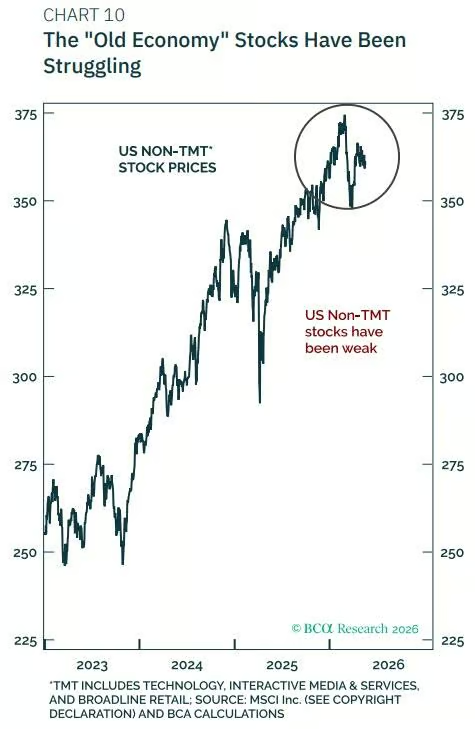

The Other 493: Still Below February

Strip out Technology and Communication Services and US share prices remain well below their February all-time high. The headline index recovery has been entirely a Mag-7 story — 493 companies are still underwater.

Source: Goldman Sachs

The Beautiful Debt

Bond Bears End in Crisis

Over the past 40 years, every bear market in US bonds ended only after major economic or financial turmoil forced a turn. Inflation expectations at 3.9% long-run with debt projected to 140% of GDP

Source: Deutsche Bank

Vol Knows Something

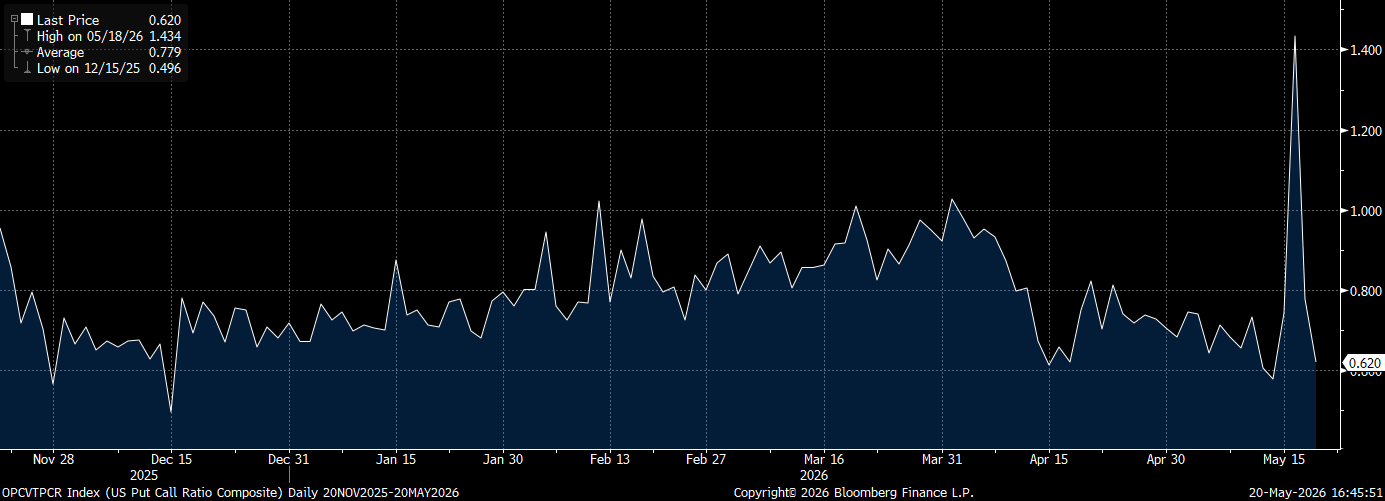

Put/Call: Back to Complacency

The put/call ratio spiked to 1.434 on May 18 — the Moody's downgrade day — then collapsed to 0.620 within three sessions. The fastest put/call reversion from fear back to complacency this year, with macro risk still fully in play.

Source: Bloomberg

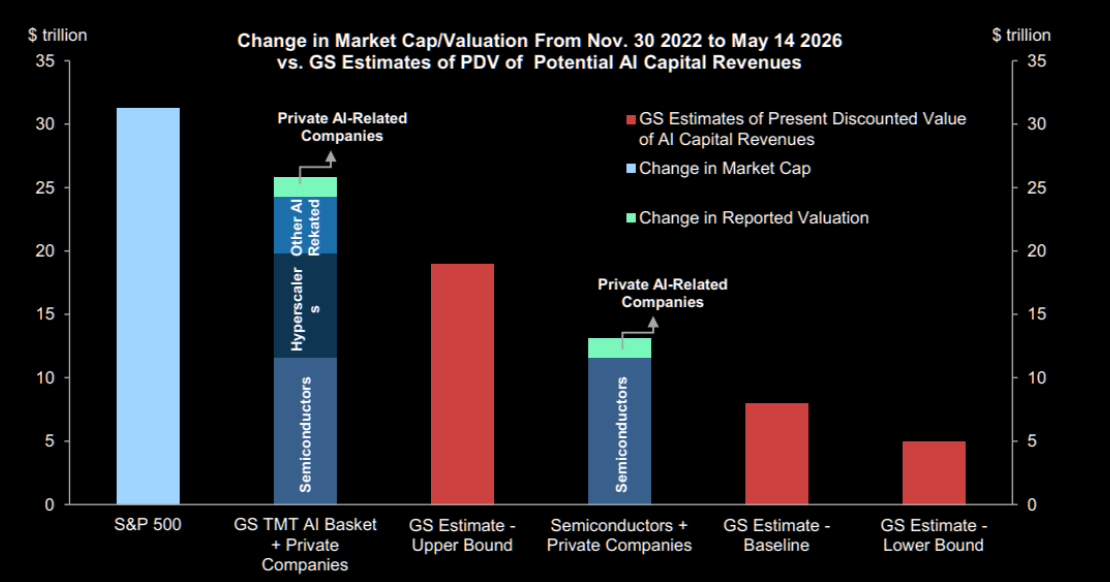

The AI Landgrab

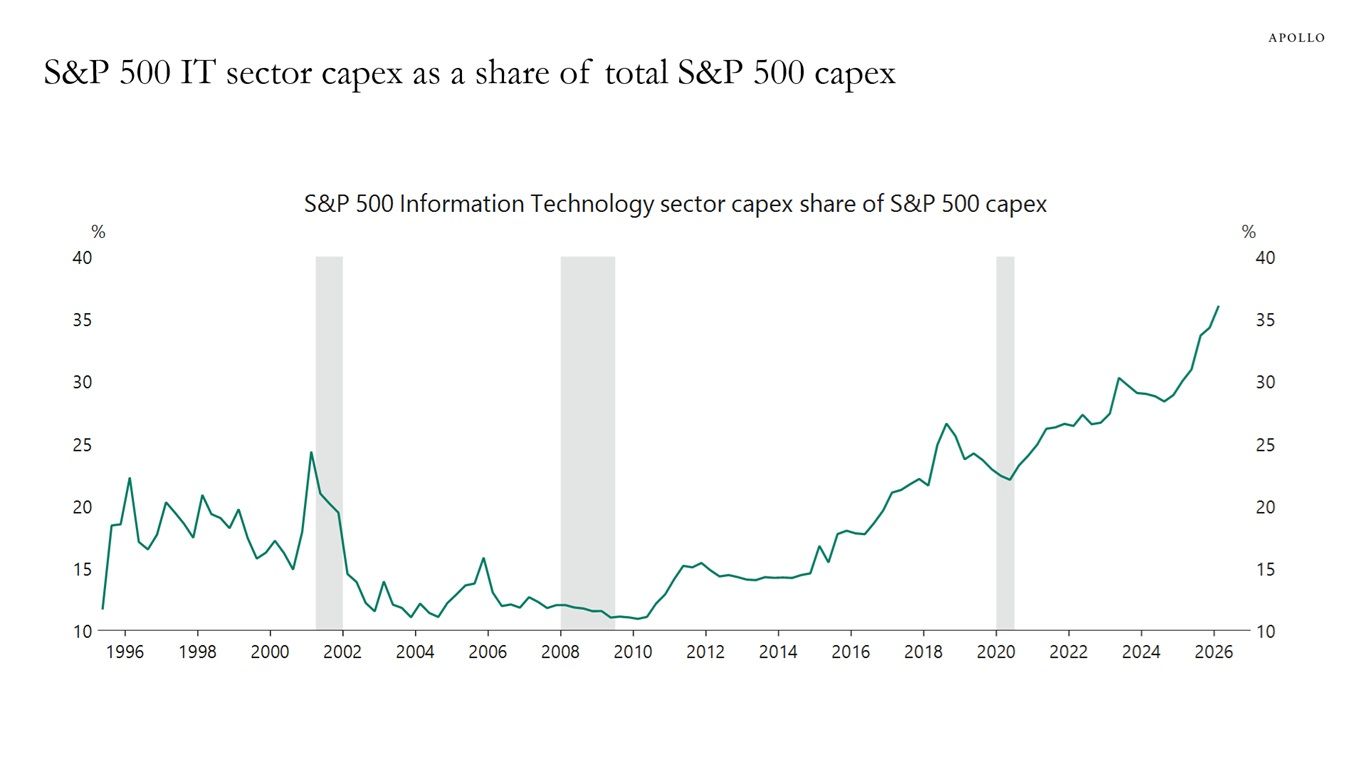

IT Capex: 35% of S&P, a Record

The S&P 500 IT sector now accounts for 35% of the index's total capital expenditure — a new all-time high as hyperscalers build out AI infrastructure at unprecedented scale. The same companies cutting the most jobs are directing every dollar of new capex into AI.

Source: Goldman Sachs

81K Jobs Cut, $725B Pledged

81,747 tech workers were laid off in Q1 2026 — double Q4 2025 and +580% vs Q4 2024 — simultaneously with $725B in hyperscaler AI capex pledges for the year. The companies doing the most cutting are the ones spending the most on AI. The capital is going to compute, not people.

Source: Goldman Sachs

$DRAM: Fastest ETF in History

The $DRAM ETF crossed $6.5B in assets in just 36 days — beating Bitcoin's IBIT record of 43 days and every other ETF launch in history. The fastest AUM ramp ever recorded is a semiconductor-memory product at the peak of an AI infrastructure cycle.

Source: EPFR

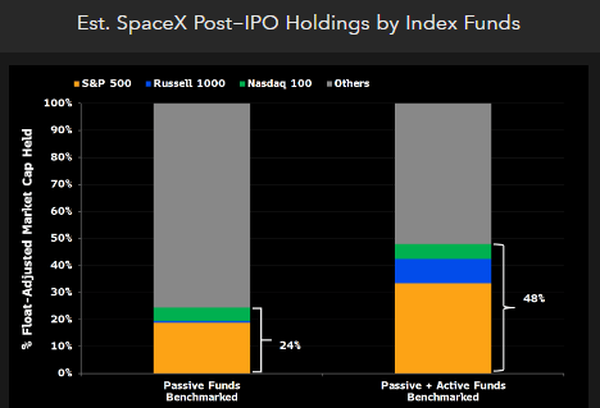

SpaceX IPO: 19% Forced Buying

Passive S&P 500 funds would need to buy roughly 19% of all public SpaceX shares within six months of IPO under fast-tracking rules — SpaceX would enter as the 6th largest index constituent. Russell 1000 and Nasdaq 100 would add another 5.5% within weeks. That's structural forced demand, not investor choice.

Source: Goldman Sachs

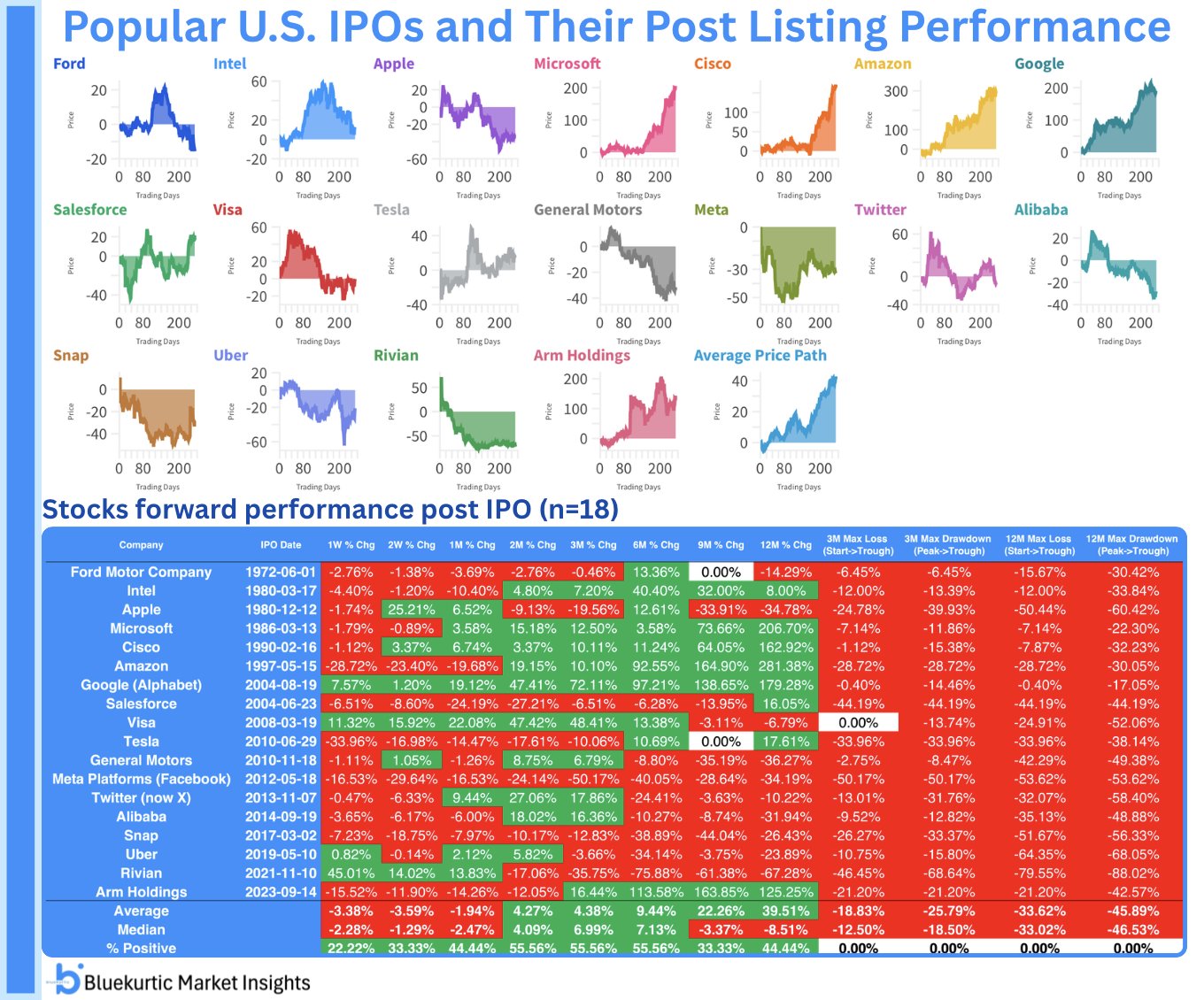

IPO Caution: Median 18.5% Drawdown

Across major US IPOs, the median 3-month maximum drawdown is 18.5% post-listing. The average 12-month return is +40% but the median is far lower. For SpaceX and OpenAI at expected valuations north of $300B, the 'everyone wins' scenario has narrow historical precedent.

Source: BofA

Just Because...

Lobster Was Peasant Food — Then Marketing Won

In colonial America, lobster was so abundant and unglamorous that it was used as fertilizer, fed to prisoners, and eaten only by the poor. Massachusetts servants actually negotiated contracts specifying they couldn't be served lobster more than 3 times a week. It wasn't until the railroad era and clever marketing by 19th-century restaurants that lobster became a luxury item.