RIA Ideas - Hedge when you can, not when you have to

Buffer Note

Elevated rates and collapsed vol at the same time — for the SPX/INDU buffer note, this is the setup.

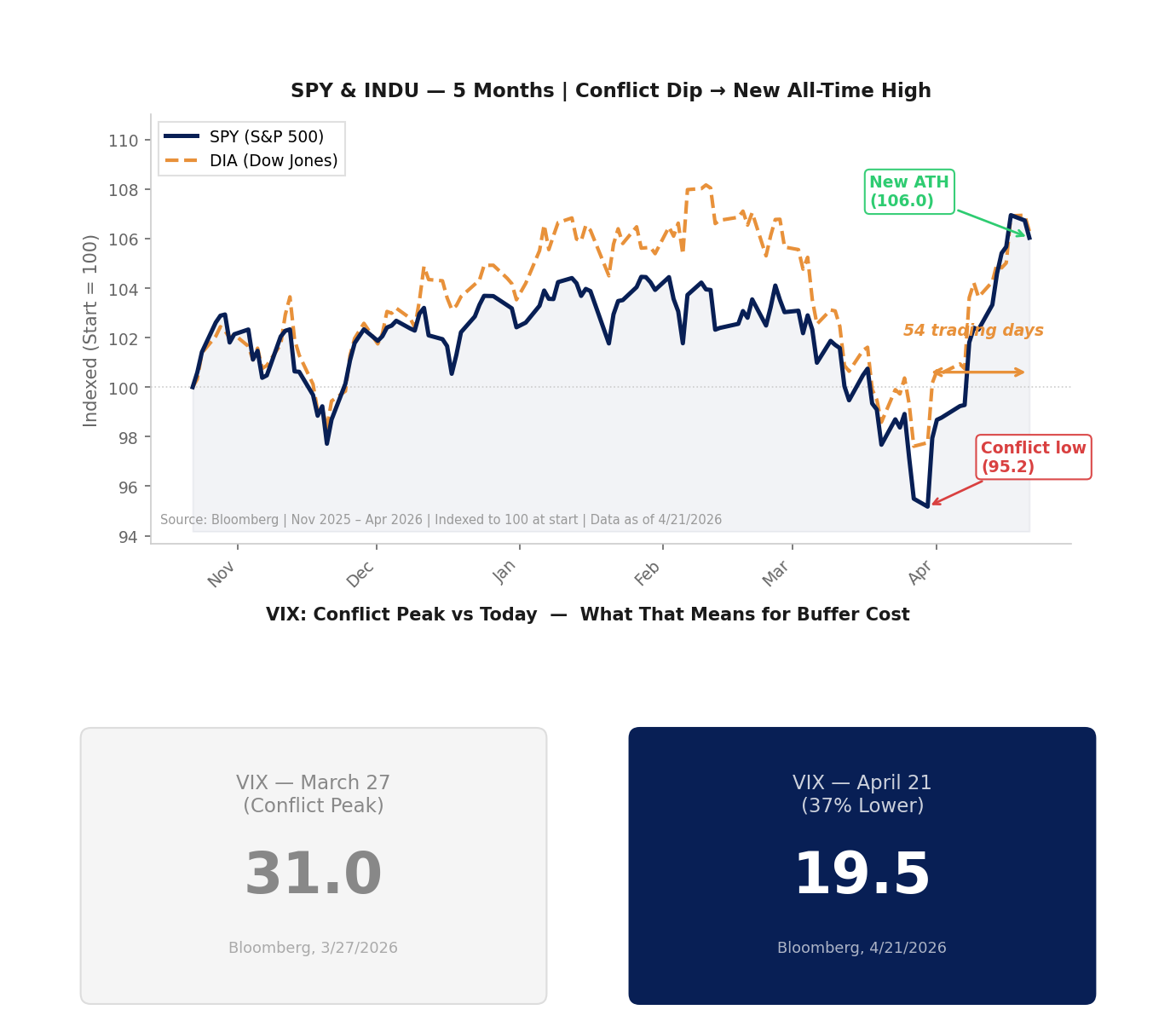

The S&P went from -9% to a new all-time high in just 54 trading days — one of the fastest reversals since 1950. The conflict pushed rates up. The resolution brought vol down. VIX dropped from 31 on March 27 to 19.5 today — a 37% move in less than four weeks.

Here's what most advisors miss: lower vol doesn't make downside protection cheaper — it makes the upside participation cheaper. The calls that give you 100% exposure to S&P gains cost less to engineer. Meanwhile, rates remaining elevated means the zero coupon bond that returns your principal at maturity requires less capital — leaving more budget for the buffer. Both things are working in your favor right now.

SPY 6 Months + VIX: Conflict Peak vs Today

Data sourced from Bloomberg as of 4/21/2026 · marinelayeradvisors.com/insights

One Way To Stay Invested With a Cushion

WoF SPX/INDU · 4 Years · 20% Hard Buffer · 130% Upside Participation

Indicative — respond back and I'll get current terms from desk.

Respond back to get more color.

Sanj

Sanjay Tolia |

Securities offered through Institutional Securities Corp. 3500 Oaklawn Ave. Ste. 400 Dallas, TX 75219 |

This material is for informational purposes only and does not constitute a recommendation. Data sourced from Bloomberg and public sources and has not been independently verified. Past performance is not indicative of future results. Structured notes involve risks including potential loss of principal. Buffer notes provide limited downside protection only — losses beyond the buffer are borne by the investor. VIX and options data referenced are indicative and do not represent actual structured note pricing. Structured note pricing is subject to issuer credit risk, market conditions, and availability at time of execution.