RIA Ideas - What hasn't ran up?

Income Note — XLF & XHB

If an income note doesn’t pay you on the upside, why pair it with what’s already run?

With an autocall income note, your upside is capped at the coupon — you don’t participate in a run-up. Which puts the focus on the downside: how far is today’s price from the barrier? A 70% barrier on an underlier already down 19% from its highs may offer a deeper effective cushion than the same barrier on something that just ran +50% in 90 days. The barrier measures from today, not from the high.

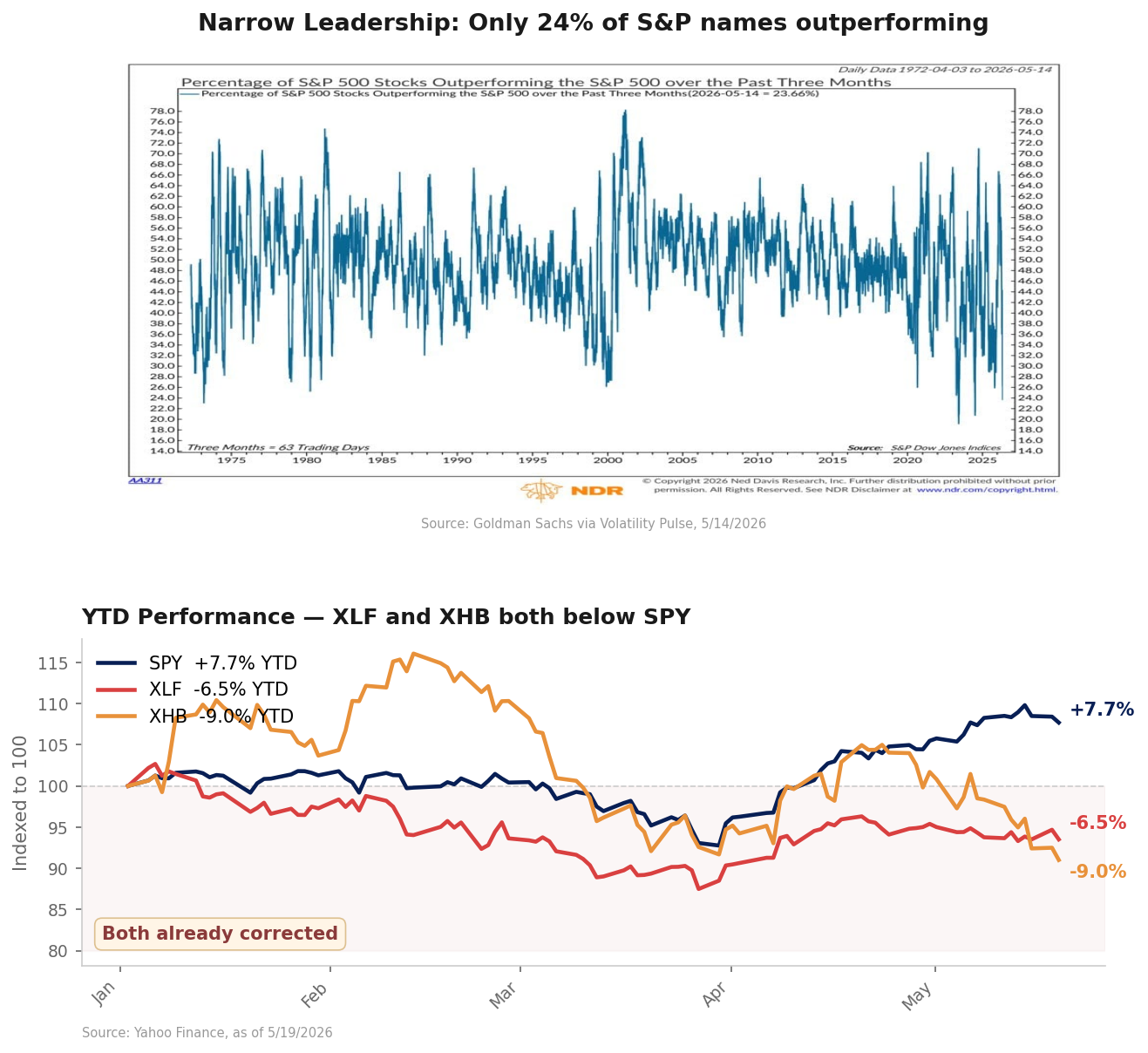

Only 22–24% of S&P 500 members outperformed the index over the past 3 months — among the lowest breadth readings since 1996 (Goldman Sachs via Volatility Pulse, 5/14/2026). Two AI names are carrying the index; the rest has already corrected. XLF: -6.5% YTD, 16.5x trailing P/E. XHB: -9.0% YTD, -19.3% over 3 months, 16.5x (Yahoo Finance, as of 5/19/2026). Both sit in the “everyone else” bucket. For income notes, underliers that have already corrected may be worth considering as inputs.

Narrow Leadership: 24% Breadth + XLF and XHB Both Below SPY YTD

Goldman Sachs · Yahoo Finance, as of 5/19/2026 · marinelayeradvisors.com/insights

One Way To Express This View

3-Year XLF & XHB Worst-Of Income

~12.5% P.A.

6 month no call · Quarterly call · 70% EKI · Quarterly pay

Two underliers, not three.

The standard income worst-of is a 3-name basket (e.g., SPX/NDX/RTY). Pairing only two underliers may reduce the risk of a single underlier breaching a barrier alone. Both XLF and XHB are already off their highs at ~16.5x trailing P/E.

Indicative levels only.

Respond back to get more color.

This material is for informational purposes only and does not constitute a recommendation. Data sourced from public sources (Yahoo Finance, Bloomberg, Goldman Sachs) and has not been independently verified. Past performance is not indicative of future results. Structured notes involve risks including potential loss of principal. Worst-of barrier notes pay a coupon contingent on each underlier and pay back principal based on the worst-performing underlier; if any single underlier breaches its barrier at maturity, principal loss is one-for-one with that underlier. Final pricing subject to market conditions and issuer availability at time of execution.