RIA Ideas - Stay long without being all in on AI

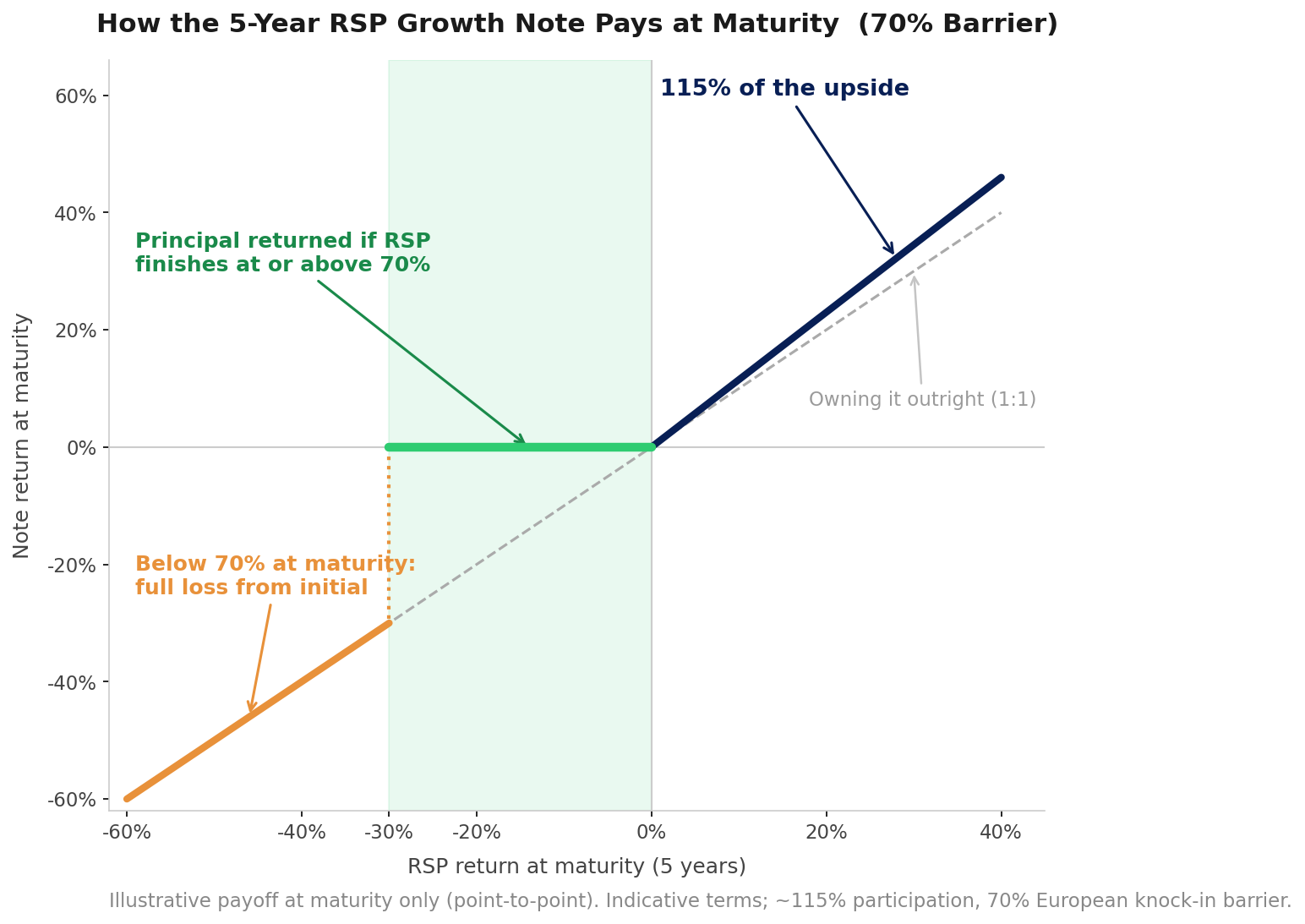

Buffered Growth Note — RSP (Equal Weight S&P 500)

How to stay long the market without being all-in on AI.

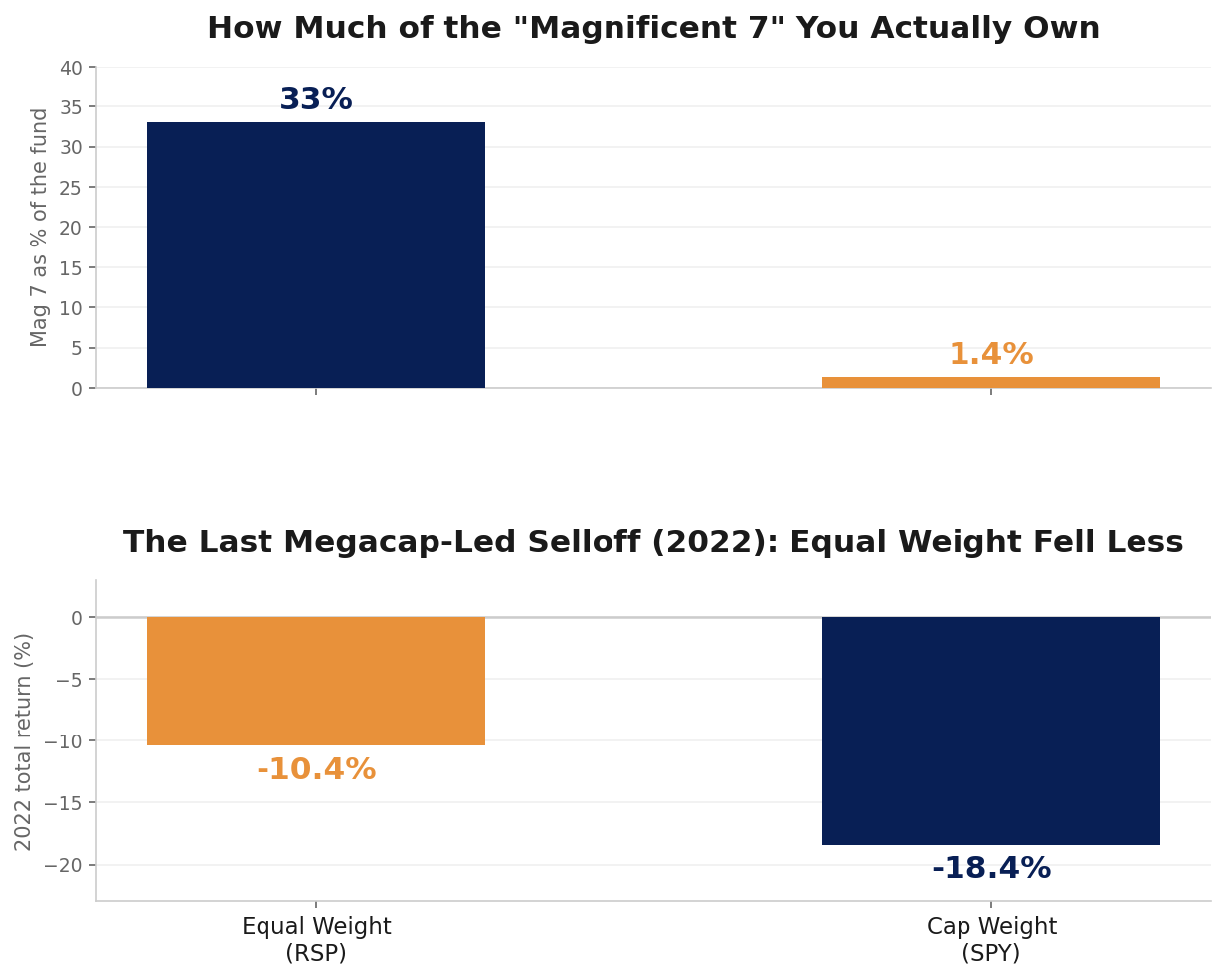

Owning the S&P 500 today is a bigger AI bet than most realize: the Magnificent 7 are ~33% of the index and semiconductors alone ~19.7% (Bloomberg/S&P Global via Citadel Securities, mid-2026). Equal weight holds the same 500 companies — but each at ~0.2%, so the Mag 7 shrink to ~1.4%. Same market, a fraction of the AI concentration.

And it may matter most when it counts. When the megacaps have been the ones to crack, equal weight has held up better — in the 2022 selloff it fell -10.4% vs -18.4% for the cap-weighted S&P, and in the 2000–02 dot-com unwind it beat cap weight by ~33 points (S&P Global). It tends to cushion most exactly when concentration reverses. A buffered RSP note may let clients stay fully long — with far less AI — and a cushion under them.

A fraction of the Mag 7 exposure — and less pain when the megacaps last cracked

Returns data: Yahoo Finance, as of 7/6/2026 · marinelayeradvisors.com/insights

One Way To Own Equal Weight

5-Year RSP Point-to-Point Growth Note

~115% Upside Participation

RSP (equal-weight S&P 500) · 5-year · point-to-point · 70% barrier (observed at maturity)

Indicative levels only.

Here’s how the note pays at maturity:

Curious how concentrated your clients’ “index” exposure really is?

This material is for informational purposes only and does not constitute a recommendation. Data sourced from public sources (Mag 7 and semiconductor index weights: Bloomberg/S&P Global via Citadel Securities, mid-2026; 2022 and YTD returns: Yahoo Finance; dot-com-era equal-weight outperformance: S&P Dow Jones Indices) and has not been independently verified. Past performance is not indicative of future results. Structured notes involve risks including potential loss of principal. A growth note with a knock-in barrier provides contingent protection only — if RSP finishes below the 70% barrier at maturity, the investor is exposed to the full decline from the initial level, not merely the amount beyond the barrier. Terms shown are indicative, subject to issuer credit risk, market conditions, and availability at time of execution.