RIA Ideas - A safer play on tech?

Income Note — SPX / XLC / RTY

The standard basket was built for a different market. It may be worth asking if it’s still the right one.

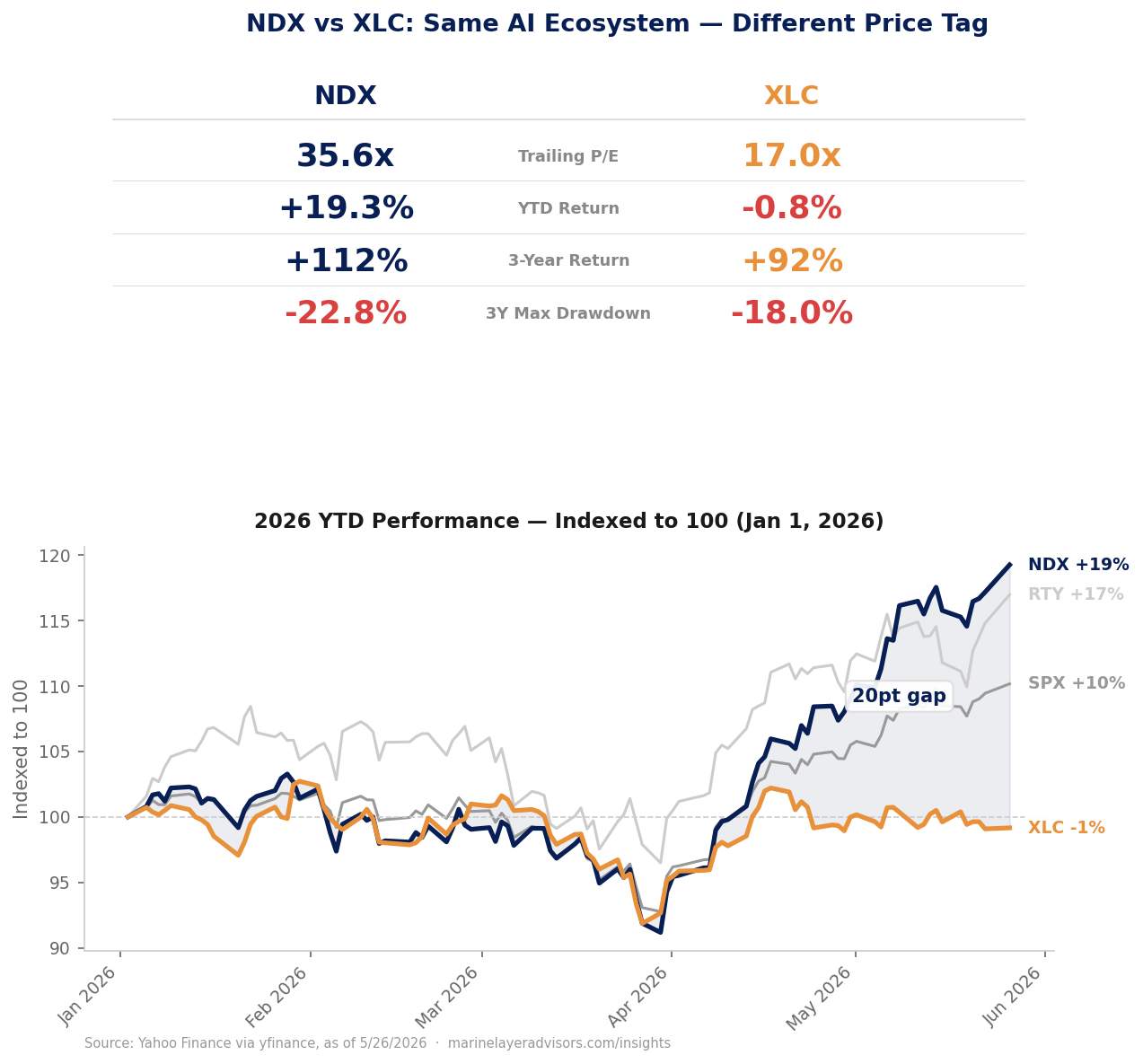

The standard worst-of basket includes NDX, which sits at 35.6x trailing P/E and is up +19.3% YTD. However, XLC (Communication Services) holds large caps like Alphabet and META — the same AI ecosystem, monetizing through ad platforms instead of chip sales — at just 17.0x trailing earnings, flat at –0.8% YTD (Yahoo Finance, 5/26/2026). Might XLC be a superior risk-adjusted replacement for NDX in certain scenarios?

For an income note, it doesn’t matter how far the underlying has run — the coupon is your ceiling. The only thing that matters is whether any underlier breaches the barrier at maturity. Max drawdown over the last 3 years: NDX –22.8%, XLC –18.0%.

Yahoo Finance · as of 5/26/2026 · marinelayeradvisors.com/insights

The Idea In Action

Standard — 3-Year SPX / NDX / RTY

~10.75% P.A.

Quarterly call at 100% · 70% barrier · Quarterly coupon

The Swap — 3-Year SPX / XLC / RTY

~10.25% P.A.

Quarterly call at 100% · 70% barrier · Quarterly coupon

NDX (35.6x P/E) swapped for XLC (17.0x P/E). Is 50 bps in yield worth the change in risk profile for some clients?

Indicative levels only.

This is the sort of analysis we automatically run for our partners. Email us back for a free analysis to see how we may be able to help.

This material is for informational purposes only and does not constitute a recommendation. Data sourced from public sources (Yahoo Finance) and has not been independently verified. Past performance is not indicative of future results. Structured notes involve risks including potential loss of principal. Worst-of barrier notes pay a coupon contingent on each underlier staying above its barrier; if any single underlier breaches its barrier at maturity, principal loss may be one-for-one with that underlier’s decline. Final pricing subject to market conditions and issuer availability at time of execution.