RIA Ideas - Defensive and Diversifying Income

Income Note — XLF / XLP / XLV

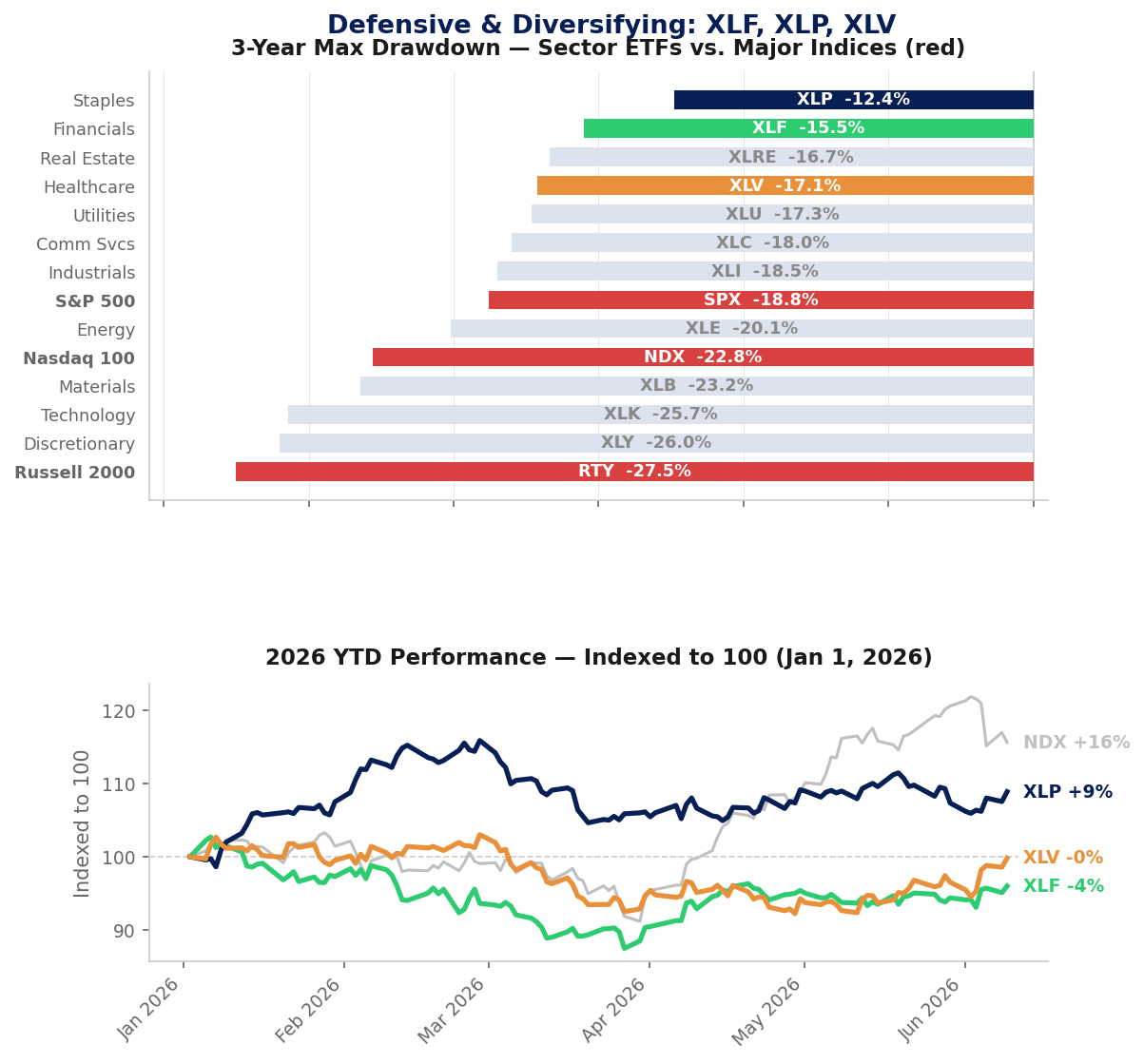

Nine percent. No NDX. No SPX. No RTY.

Consumer Staples (XLP), Financials (XLF), and Healthcare (XLV) posted the three smallest 3-year max drawdowns of any major S&P 500 sector — XLP at –12.4%, XLF at –15.5%, and XLV at –17.1% (Yahoo Finance, 6/9/2026). None of them are the indices that typically show up in a worst-of income note.

For an income note, the coupon is your ceiling — you don’t participate in the upside. The only question is whether any underlier breaches its barrier at maturity. Here’s the part that stands out: over the last three years, all three of these sectors held up better than the indices these notes usually run on — the S&P 500 gave back –18.8%, the Nasdaq 100 –22.8%, and the Russell 2000 –27.5%. A 70% barrier on underliers that have each stayed within 18% of their peak may offer a different risk starting point.

Yahoo Finance · as of 6/9/2026 · marinelayeradvisors.com/insights

The Idea

3-Year XLF / XLP / XLV Worst-Of

~9% P.A.

Quarterly call at 70% · 70% barrier · Quarterly coupon · 3-month non-call

No NDX. No SPX. No RTY. Just the three sectors that have historically held their ground the most. Could this be worth exploring for clients looking for income with a different risk starting point?

Indicative levels only.

This is the sort of analysis we automatically run for our partners. Email us back for a free analysis to see how we may be able to help.

This material is for informational purposes only and does not constitute a recommendation. Data sourced from public sources (Yahoo Finance) and has not been independently verified. Past performance is not indicative of future results. Structured notes involve risks including potential loss of principal. Worst-of barrier notes pay a coupon contingent on each underlier staying above its barrier; if any single underlier breaches its barrier at maturity, principal loss may be one-for-one with that underlier’s decline. Final pricing subject to market conditions and issuer availability at time of execution.